Self-Employed Borrowers in Tampa Bay: Advanced Underwriting Strategies Most Banks Still Get Wrong

Why Traditional Lenders Struggle with Variable Income in Florida

Tampa Bay is a thriving hub for entrepreneurs, freelancers, and small business owners. However, when it comes time to purchase a home, many self-employed professionals discover a frustrating reality: traditional banks simply do not understand variable income. Standard underwriting guidelines are built around predictable W-2 paychecks. If you run a business, you likely take advantage of legal tax deductions to minimize your liability. While this is a smart business strategy, it artificially lowers your net income on paper, which can lead to rapid mortgage denials from big-box lenders.

At The Orlicki Group, we know that your tax returns do not always tell the full story of your financial health. As an independent mortgage broker in Tampa, we specialize in finding tailored solutions that big banks overlook. We work on your behalf to present your true cash flow to lenders who understand the nuances of self-employment. By leveraging advanced underwriting strategies, we help local business owners secure the financing they deserve without the standard institutional roadblocks.

Unlocking Homeownership with Non-QM and Bank Statement Loans

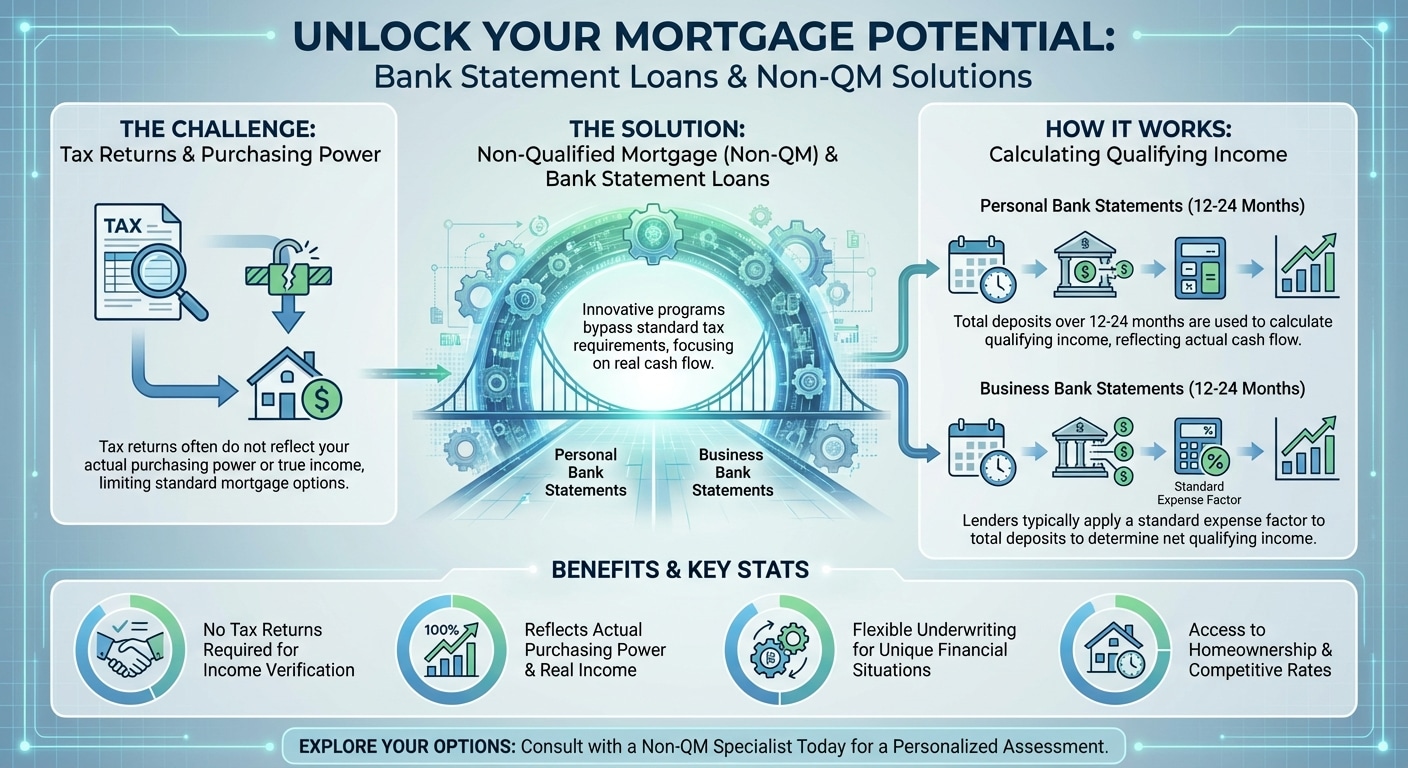

If your tax returns do not reflect your actual purchasing power, you are not out of options. The solution lies in Non-Qualified Mortgage (Non-QM) products, specifically bank statement loans. These innovative programs bypass standard tax return requirements and instead calculate your qualifying income based on the total deposits into your personal or business bank accounts over a 12 to 24-month period.

- Business Bank Statements: Lenders typically use a standard expense factor to calculate your net qualifying income from gross deposits.

- Personal Bank Statements: Lenders look at 100% of the deposits transferred from your business to your personal accounts.

- 1099 Income Loans: Perfect for independent contractors, these loans use your 1099 forms rather than complex tax returns.

Because we are not tied to a single bank, our team shops around our network of top lenders to find the most competitive home loan options for your unique scenario. This flexibility allows us to secure lower rates, offer faster turn times, and provide the expert guidance necessary to navigate the competitive Tampa Bay real estate market.

| Feature | Traditional Mortgage | Bank Statement Loan (Non-QM) |

|---|---|---|

| Income Verification | W-2s, Pay Stubs, Tax Returns | 12-24 Months of Bank Statements |

| Tax Returns Required | Yes (Typically 2 years) | No |

| Ideal Borrower | Salaried Employees | Entrepreneurs, Freelancers, 1099 Workers |

| Approval Speed | Standard | Often Faster for Self-Employed |

Expert Tactics to Position Your Mortgage Application for Success

Securing a self-employed mortgage in Florida requires a proactive approach. To position yourself for the best possible rates and terms, you need to prepare your financial profile before you ever submit an application. Here are a few advanced tactics to ensure a smooth underwriting process:

- Separate Business and Personal Finances: Commingling funds is a major red flag for underwriters. Keep strict boundaries between your business operating accounts and your personal checking accounts.

- Maintain Consistent Deposits: Lenders look for stability. Avoid large, unexplained cash deposits, and try to maintain a steady flow of income into your primary accounts.

- Consult a Mortgage Broker Early: Do not wait until you find a house to figure out your financing. Use our mortgage calculator to estimate your budget, and get pre-approved early.

Our mission is to educate and advocate for you throughout the entire process. Whether you are a first-time homebuyer or an experienced investor, we encourage you to download our Mortgage Walkthrough Guide to learn exactly what happens at every step of your journey.

Q1: What is a bank statement loan for self-employed borrowers in Tampa?

A bank statement loan is a type of Non-QM mortgage that allows self-employed individuals to qualify for a home loan using their personal or business bank deposits over 12 to 24 months, rather than relying on tax returns.

Q2: Do I need tax returns to get a mortgage if I own a business?

Not necessarily. While traditional conventional loans require tax returns, independent mortgage brokers can offer alternative loan products like bank statement loans or 1099 loans that do not require tax returns for approval.

Q3: How long do I need to be self-employed to qualify for a Non-QM loan?

Most lenders require you to have been self-employed for at least two years. However, depending on your industry experience and financial strength, some specialized lenders may allow for exceptions with just one year of self-employment.

Q4: Are interest rates higher for self-employed mortgages?

Non-QM loans generally carry slightly higher interest rates than standard conventional loans due to the alternative documentation used. However, working with an independent broker allows you to shop multiple lenders to secure the most competitive rate available.

Q5: Why should I use a Tampa mortgage broker instead of my local bank?

A local bank only offers its own limited loan products, which often exclude self-employed borrowers with variable income. An independent broker like The Orlicki Group works for you, shopping dozens of lenders to find flexible options, lower rates, and tailored solutions.

Ready to Secure Your Next Mortgage?

Don’t let variable income keep you from your dream home. Get honest, open, and expert guidance tailored to your unique financial picture.

Call Us: (813) 302-1616 Email: info@orlickigroup.com