Jumbo Loans in the Tampa Bay Luxury Segment: Structuring for Success in 2026

Navigating the High-End Tampa Real Estate Market

The Tampa Bay luxury real estate market continues to experience unprecedented growth as we move into 2026. For high-net-worth individuals eyeing waterfront estates in South Tampa, sprawling properties in Avila, or modern penthouses downtown, securing the right financing is just as critical as finding the perfect property. This is where a strategically structured jumbo loan becomes a powerful financial tool.

Unlike conventional mortgages, jumbo loans exceed the conforming loan limits set by the Federal Housing Finance Agency (FHFA). Because these loans cannot be purchased by Fannie Mae or Freddie Mac, lenders carry more risk, making the underwriting process more rigorous. However, partnering with an experienced Tampa mortgage broker like The Orlicki Group opens the door to flexible terms, competitive rates, and customized solutions tailored to complex financial portfolios.

- Preserve Liquidity: Keep your capital invested in high-yield assets rather than tying it up in a massive down payment.

- Flexible Underwriting: Asset dissipation and bank statement loan options cater to self-employed and high-net-worth borrowers.

- Local Expertise: Navigating Tampa-specific property requirements, including flood zones and luxury condo association rules.

Strategic Loan Structuring for High-Net-Worth Borrowers

When dealing with higher-value properties, standard mortgage solutions simply do not work. High-net-worth clients often have complex income structures, including restricted stock units (RSUs), K-1 income, trust distributions, and multiple business entities. Successfully securing a jumbo loan in Tampa requires a mortgage broker who understands how to present these financial profiles in the best possible light.

At The Orlicki Group, Oliver Orlicki (NMLS #205123) and his team specialize in creative financing. Here are the top strategies for structuring a jumbo loan for success in 2026:

- Asset-Based Lending: Instead of relying solely on traditional W-2 income, borrowers can qualify by demonstrating substantial liquid assets. Lenders can calculate a monthly income stream based on asset depletion, which is ideal for retirees or investors.

- Cross-Collateralization: Leverage equity from another luxury property in your portfolio to secure favorable terms on your new Tampa Bay home without liquidating current investments.

- Optimizing Cash Reserves: Jumbo lenders typically require significant cash reserves, often 12 to 24 months of mortgage payments. Structuring your portfolio to show accessible liquidity can drastically improve your rate and approval odds.

By working with an independent broker rather than a traditional retail bank, you gain access to a wider network of private investors and portfolio lenders who offer the flexibility that high-end transactions demand.

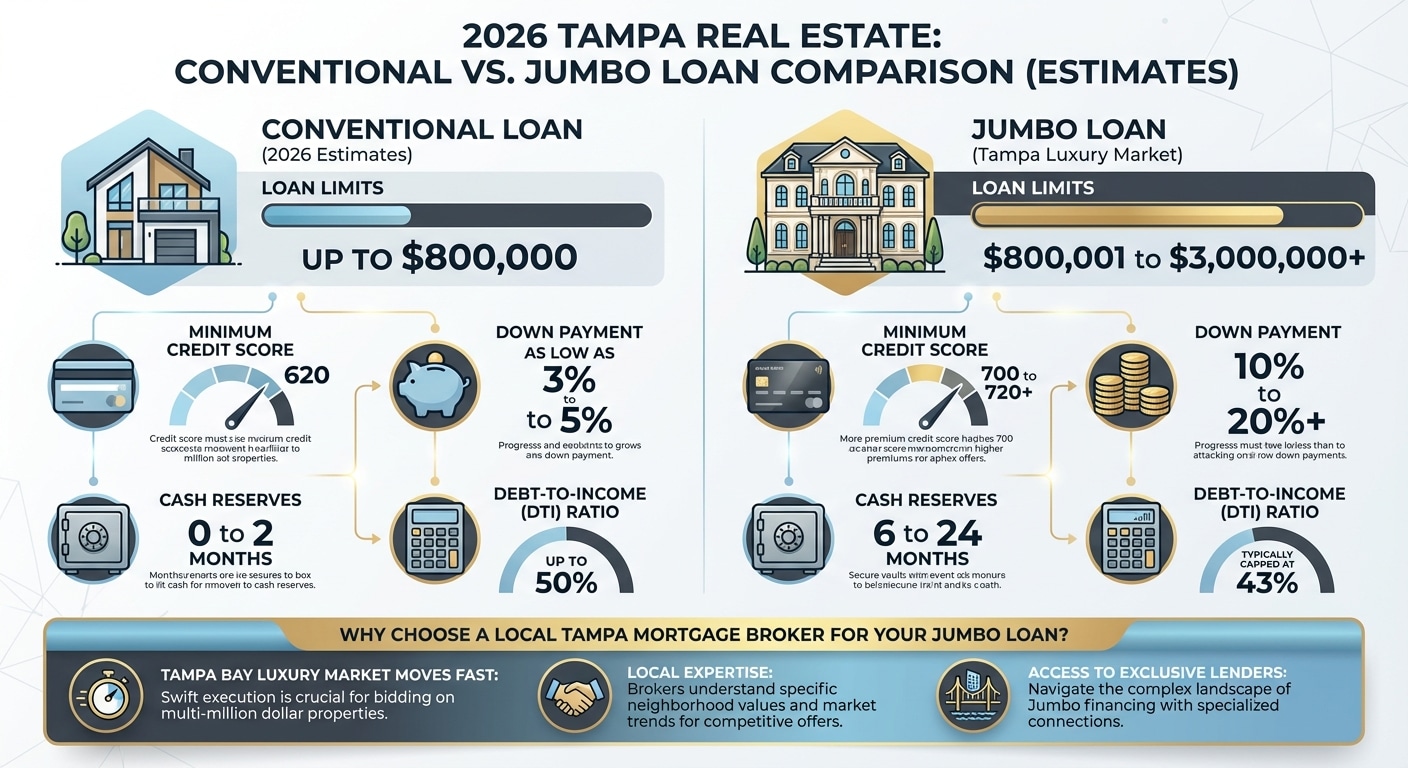

| Loan Requirement | Conventional Loan (2026 Estimates) | Jumbo Loan (Tampa Luxury Market) |

|---|---|---|

| Loan Limits | Up to $800,000 | $800,001 to $3,000,000+ |

| Minimum Credit Score | 620 | 700 to 720+ |

| Down Payment | As low as 3% to 5% | 10% to 20%+ (varies by lender) |

| Cash Reserves | 0 to 2 months | 6 to 24 months |

| Debt-to-Income (DTI) Ratio | Up to 50% | Typically capped at 43% |

Why Choose a Local Tampa Mortgage Broker for Your Jumbo Loan?

The Tampa Bay luxury real estate market moves fast. Whether you are bidding on a multi-million dollar estate in Davis Islands or a beachfront property in Clearwater, having a pre-approval from a reputable, locally trusted broker is your strongest asset. Big banks are notorious for slow underwriting and rigid guidelines, which can cost you the home of your dreams in a competitive market.

As an independent mortgage broker, The Orlicki Group works for you, not the bank. We shop your scenario across a vast network of top lenders to find the absolute best rates, lowest fees, and most accommodating terms for your specific situation. Ready to take the next step? Contact Oliver Orlicki directly at 1-813-302-1616 or email info@orlickigroup.com to discuss your luxury financing needs.

Compliance and Legal Notice: The Orlicki Group is an Equal Housing Lender. Oliver Orlicki, Mortgage Loan Originator, NMLS #205123. All loans are subject to credit and property approval. Rates, program terms, and conditions are subject to change without notice. Not all products are available in all states or for all amounts.

Q1: What qualifies as a jumbo loan in Tampa, FL for 2026?

A jumbo loan is any mortgage that exceeds the conforming loan limits set by the FHFA. For 2026, this typically means loan amounts exceeding the estimated $800,000 threshold in Hillsborough and Pinellas counties, though exact limits update annually.

Q2: Can I get a jumbo loan with a 10% down payment?

Yes, while traditional jumbo loans often require a 20% down payment, The Orlicki Group works with specialized portfolio lenders who offer 10% down payment options for highly qualified borrowers with excellent credit and sufficient reserves.

Q3: How do cash reserves work for high-net-worth mortgages?

Lenders usually require jumbo borrowers to hold 6 to 24 months of mortgage payments in liquid or semi-liquid accounts. This acts as a safety net and compensates for the higher risk of a large loan amount.

Q4: Can self-employed individuals qualify for luxury home financing?

Absolutely. We offer bank statement loans and asset dissipation programs that allow self-employed borrowers and business owners to qualify using alternative income documentation rather than standard tax returns.

Q5: Why should I use a mortgage broker instead of my primary bank for a jumbo loan?

A broker like The Orlicki Group has access to dozens of lenders, including private banks and wholesale investors. This means more flexible underwriting guidelines, faster closing times, and highly competitive rates tailored to complex financial situations.