For many potential homebuyers in the Sunshine State, the biggest hurdle standing between renting and owning is the down payment. With home prices rising in areas like Tampa, St. Petersburg, and Sarasota, saving up 20%—or even 3.5%—can feel like a mountain to climb.

But what if you didn’t need a down payment at all?

Enter the USDA Loan. Often misunderstood as a program strictly for farmers, the USDA Rural Development loan is actually one of the most powerful tools available for everyday homebuyers in Florida. It offers 100% financing, competitive interest rates, and lower mortgage insurance costs than many other loan types.

At The Orlicki Group, we specialize in helping Florida families navigate the mortgage landscape. Whether you are a first-time homebuyer in Tampa or looking to relocate to a quieter part of Pasco County, this guide will walk you through everything you need to know about USDA loans in Florida.

What is a USDA Loan?

A USDA loan is a mortgage backed by the U.S. Department of Agriculture. The program was created to boost homeownership and economic development in rural and suburban areas. Because the government guarantees a portion of the loan, lenders like The Orlicki Group can offer more favorable terms to borrowers who might not fit the strict mold of conventional financing.

The most distinct feature of this loan is that it allows you to finance 100% of the home’s purchase price. This means zero money down is required from your own pocket for the down payment.

Dispelling the “Farmer” Myth

Let’s clear up the biggest misconception right away: You do not need to be a farmer, buy a farm, or grow crops to qualify for a USDA loan.

In Florida, “rural” is defined much more broadly than you might think. Many suburban areas on the outskirts of major cities like Tampa, Orlando, and Jacksonville are eligible. If you are looking for a home in a town with a population under 35,000, there is a high probability the property qualifies.

Key Benefits of Florida USDA Loans

Why should you consider a USDA loan over an FHA or Conventional loan? Here are the standout benefits:

- Zero Down Payment: This is the only mainstream government-backed loan (aside from VA loans for veterans) that requires $0 down.

- Low Mortgage Insurance: USDA loans require an upfront guarantee fee and an annual fee (paid monthly). However, these fees are significantly lower than FHA mortgage insurance premiums (MIP) and often lower than Private Mortgage Insurance (PMI) on conventional loans.

- Competitive Interest Rates: Because the loan is government-guaranteed, lenders can often offer lower rates, even to borrowers with average credit scores.

- Flexible Credit Guidelines: While standards exist, USDA loans can be more forgiving regarding credit history than conventional mortgages.

- Seller Concessions: The seller can contribute up to 6% of the sales price toward your closing costs, potentially minimizing your out-of-pocket expenses even further.

USDA Loan Requirements in Florida

While the benefits are incredible, USDA loans do have specific eligibility requirements. These are generally divided into three categories: Credit, Income, and Property.

1. Credit and Employment History

To qualify, lenders generally look for a credit score of 640 or higher for the automated underwriting system. However, if your score is lower, do not count yourself out. At The Orlicki Group, we have access to lenders who can perform manual underwriting for borrowers with credit scores down to 600 or those with non-traditional credit references (like rental history or utility payments).

You must also demonstrate a stable employment history, typically showing two years of consistent income.

2. USDA Income Limits

The USDA program is designed for low-to-moderate-income households. Consequently, there is a maximum income limit to qualify. This limit varies by county and household size.

Generally, your total household income cannot exceed 115% of the median household income for the area. It is important to note that USDA looks at the income of all adult household members, not just the person on the loan. However, there are deductions available for childcare expenses, dependents, and elderly care that can help you stay under the limit.

Need to check if your income qualifies? Contact us today for a quick analysis.

3. Property Eligibility (Location, Location, Location)

The home must be your primary residence and must be located in a USDA-eligible area. In Florida, you might be surprised by which areas qualify. While downtown Tampa or St. Petersburg won’t qualify, many rapidly growing communities just a short drive away often do.

USDA vs. FHA vs. Conventional: A Quick Comparison

Choosing the right mortgage can be confusing. Here is a breakdown of how USDA loans stack up against other popular options.

| Feature | USDA Loan | FHA Loan | Conventional Loan |

|---|---|---|---|

| Down Payment | 0% | 3.5% | 3% – 20% |

| Mortgage Insurance | Low (Guarantee Fee) | High (MIP for life of loan) | Varies (PMI drops at 20% equity) |

| Credit Score | 640+ (Flexible) | 580+ | 620+ |

| Income Limits | Yes (Max Limits) | No | No |

| Location Restriction | Yes (Eligible Areas Only) | No | No |

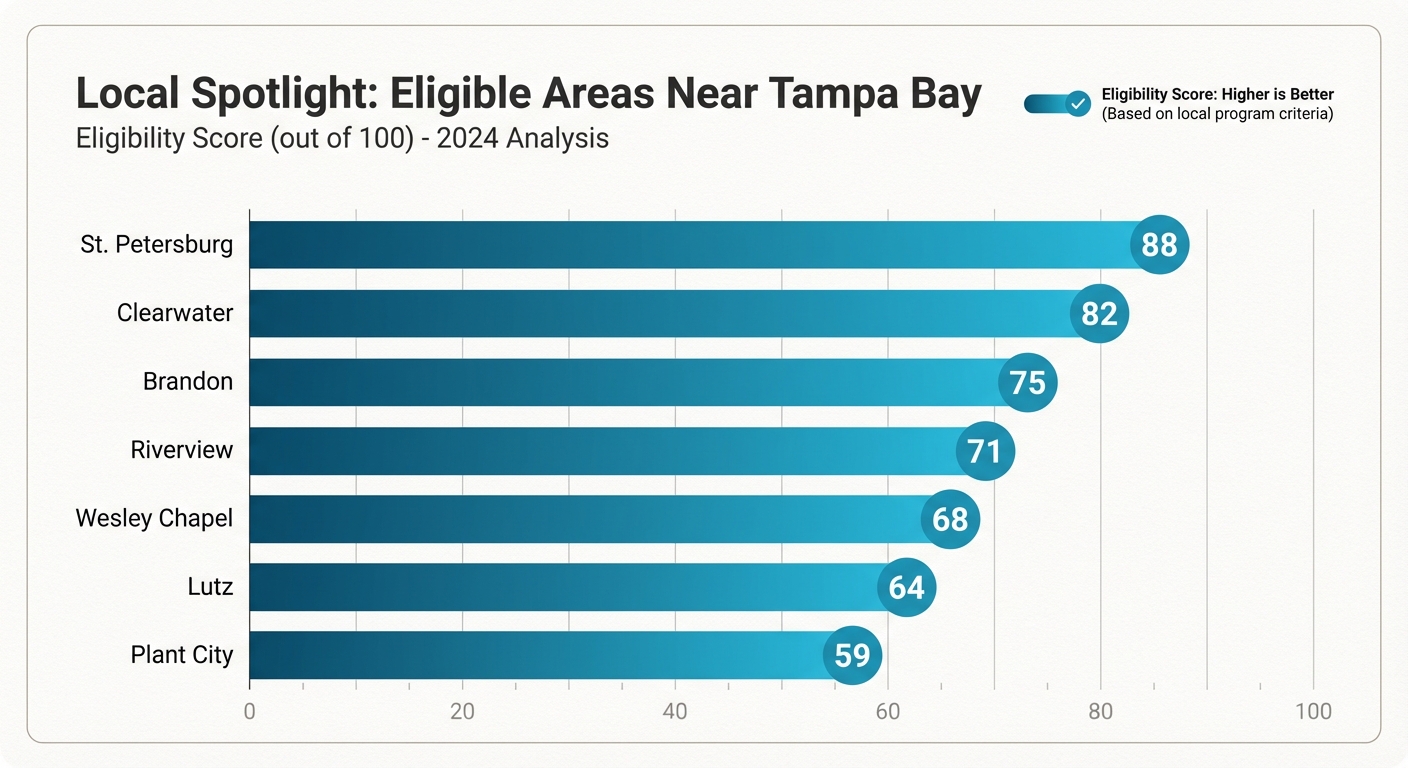

Local Spotlight: Eligible Areas Near Tampa Bay

- Pasco County: Many areas in Land O’ Lakes, Wesley Chapel, Zephyrhills, and Dade City are often eligible.

- Hillsborough County: While the city center is ineligible, outskirts like Plant City, Wimauma, and parts of Ruskin often qualify.

- Polk County: A significant portion of Polk County, including areas around Lakeland and Winter Haven, falls into USDA-eligible zones.

- Manatee & Sarasota Counties: Areas east of I-75 frequently meet the rural criteria.

Note: USDA maps change periodically. It is vital to work with a local expert like Oliver Orlicki and his team to verify specific property eligibility before you make an offer.

Why Work with The Orlicki Group?

You might be tempted to walk into a big bank to ask for a mortgage, but working with an independent mortgage broker offers distinct advantages—especially for specialized products like USDA loans.

We Work for You, Not the Bank

Expert Guidance on Complex Loans

Government loans involve specific paperwork and strict underwriting guidelines. Having an expert guide who knows the nuances of the Florida market can make the difference between a smooth closing and a denied application. We have over 24 years of experience helping buyers navigate these processes.

Fast Pre-Approvals

In a competitive market, speed matters. We offer fast pre-approvals so you can shop with confidence. Get pre-approved today to see how much home you can afford.

The USDA Loan Process: Step-by-Step

- Pre-Qualification: Contact The Orlicki Group. We will review your income, credit, and debt to determine if you meet the basic USDA criteria.

- Property Search: Once you know your budget, work with your real estate agent to find homes in USDA-eligible areas. We can provide you with a map overlay to help your search.

- Make an Offer: When you find the perfect home, make an offer. Remember, you can ask the seller to pay closing costs!

- Processing & Underwriting: Once your offer is accepted, we submit your file to the lender. USDA loans go through a two-step approval: first by the lender, and then a final sign-off by the USDA office.

- Closing: Once the USDA issues their commitment, you sign the papers and get the keys to your new home.

Frequently Asked Questions (FAQs)

1. Is there a maximum loan amount for USDA loans in Florida?

Unlike FHA or Conventional loans, USDA loans do not have a set maximum loan limit. Instead, your loan amount is limited by your debt-to-income (DTI) ratio. As long as you can afford the monthly payments based on your income and debts, you can qualify for the loan amount.

2. Can I use a USDA loan to buy a second home or investment property?

No. The USDA Single Family Housing Guaranteed Loan Program is strictly for primary residences. You must intend to live in the home as your main dwelling.

3. How long does it take to close a USDA loan?

USDA loans can take slightly longer than conventional loans because they require a secondary approval from the USDA office after the lender approves the file. However, at The Orlicki Group, we pride ourselves on efficiency. A typical closing takes 30 to 45 days.

4. Can I get a USDA loan if I have had a bankruptcy or foreclosure?

Yes, it is possible. generally, you must wait three years after a Chapter 7 bankruptcy discharge or a foreclosure before applying. For Chapter 13 bankruptcy, you may be eligible after 12 months of on-time plan payments with court permission.

5. Do USDA loans have a prepayment penalty?

No. You can pay off your USDA mortgage early or refinance it at any time without facing any prepayment penalties.

Ready to Stop Renting and Start Owning?

If you are tired of rising rents in Tampa Bay and want to explore zero-down homeownership, a USDA loan might be the perfect fit for you. Don’t let the fear of a down payment keep you from your dream home.

The Orlicki Group is here to guide you every step of the way, providing honest, open, and expert advice. Let’s see if you qualify for a Florida USDA loan today.

Call us at (813) 302-1616 or email info@orlickigroup.com to get started.

Click Here to Request Your Free Quote

Disclaimer: The Orlicki Group is an independent mortgage broker. NMLS #205123. Oliver Orlicki NMLS #205123. This content is for informational purposes only and does not constitute a commitment to lend. Loan programs, rates, and terms are subject to change without notice. Eligibility is subject to credit and property approval. Not all applicants will qualify. The Orlicki Group is an Equal Housing Opportunity provider.