When you begin the journey to homeownership in Tampa, FL, or anywhere across the Sunshine State, you will quickly encounter a variety of financing options. From government-backed FHA loans to specialized VA programs for veterans, the mortgage landscape is diverse. However, one loan type consistently reigns supreme in popularity: the conventional loan.

At The Orlicki Group, we have helped thousands of families in Tampa Bay and beyond secure the financing they need to buy their dream homes. Time and again, we see borrowers gravitating toward conventional mortgages. But why are conventional loans the most commonly used loan programs? Is it just habit, or are there distinct financial advantages?

In this comprehensive guide, we will explore the mechanics of conventional lending, why it offers superior flexibility for many borrowers, and how choosing the right loan program can impact your long-term financial health. Whether you are a first-time homebuyer in St. Petersburg or looking to refinance in downtown Tampa, understanding these loans is crucial to your success.

What Exactly is a Conventional Loan?

Before diving into the benefits, it is important to define what a conventional loan actually is. Unlike FHA, VA, or USDA loans, a conventional loan is not backed or insured by the federal government. Instead, these loans are originated by private lenders—such as banks, credit unions, and independent mortgage brokers like The Orlicki Group.

Most conventional loans are “conforming” loans, meaning they adhere to the guidelines set by two government-sponsored enterprises (GSEs): Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation). Because these loans follow strict standardization regarding credit scores, debt-to-income ratios, and loan limits, they can be sold on the secondary market, which keeps interest rates competitive for borrowers.

The Top Reasons Borrowers Choose Conventional Loans

There is a reason conventional mortgages account for the majority of home loans in the United States. They offer a blend of flexibility, lower costs for qualified borrowers, and fewer restrictions on property types. Here are the primary drivers of their popularity:

1. Cancellable Private Mortgage Insurance (PMI)

One of the most significant advantages of a conventional loan over an FHA loan is how mortgage insurance is handled. If you put down less than 20% on a home purchase, lenders typically require Private Mortgage Insurance (PMI) to protect their investment.

With an FHA loan, the mortgage insurance premium (MIP) generally stays with the loan for its entire life, regardless of how much equity you build, unless you put down a substantial amount initially. However, with a conventional loan, PMI is not permanent. Once your loan-to-value (LTV) ratio drops to 78% (or you reach 20% equity and request cancellation), the PMI is removed. This can save homeowners in Tampa hundreds of dollars a month over the life of the loan.

2. Flexibility in Property Types

Government-backed loans often come with strict property requirements. For example, FHA loans are primarily designed for primary residences and have rigorous safety and habitability standards that some fixer-uppers might not meet.

Conventional loans offer much more freedom regarding the type of real estate you can purchase. They are the standard financing vehicle for:

- Primary Residences: The home you live in.

- Second Homes: Vacation condos on the Gulf Coast or winter homes.

- Investment Properties: Rental properties and income-generating real estate.

If you are looking to build a real estate portfolio in Florida, conventional financing is often the only route for buying properties you do not intend to occupy full-time.

3. Competitive Interest Rates and Terms

For borrowers with good to excellent credit (typically 720 and above), conventional loans usually offer the lowest interest rates available. Because the lender is taking on less risk with a high-credit borrower, they reward that borrower with better pricing.

Additionally, conventional loans offer a wide array of term options. While the 30-year fixed-rate mortgage is the industry standard, borrowers can also choose:

- 15-year fixed-rate mortgages (great for saving on interest).

- 20-year or 10-year terms.

- Adjustable-Rate Mortgages (ARMs), which may offer lower initial rates.

4. Lower Down Payment Options for First-Time Buyers

A common myth is that you need a 20% down payment to get a conventional loan. This is simply not true. Thanks to programs like Fannie Mae’s HomeReady® and Freddie Mac’s Home Possible®, qualified first-time homebuyers can get into a home with as little as 3% down.

While putting 20% down helps avoid PMI, the ability to enter the market with a smaller down payment makes conventional loans accessible to a wider demographic of buyers in Tampa Bay.

Conventional vs. Government Loans: A Comparison

To help you visualize why conventional loans are often preferred, here is a comparison of conventional loans against their government-backed counterparts.

| Feature | Conventional Loan | FHA Loan | VA Loan |

|---|---|---|---|

| Target Audience | Borrowers with good credit & stable income | Borrowers with lower credit or higher debt | Veterans, Active Duty, and eligible spouses |

| Minimum Down Payment | 3% – 5% | 3.5% | 0% |

| Mortgage Insurance | PMI (Cancellable at 20% equity) | MIP (Usually permanent) | None (Funding Fee applies) |

| Credit Score Requirements | Typically 620+ | Typically 580+ | Flexible (Lender discretion) |

| Property Use | Primary, Second Home, Investment | Primary Residence Only | Primary Residence Only |

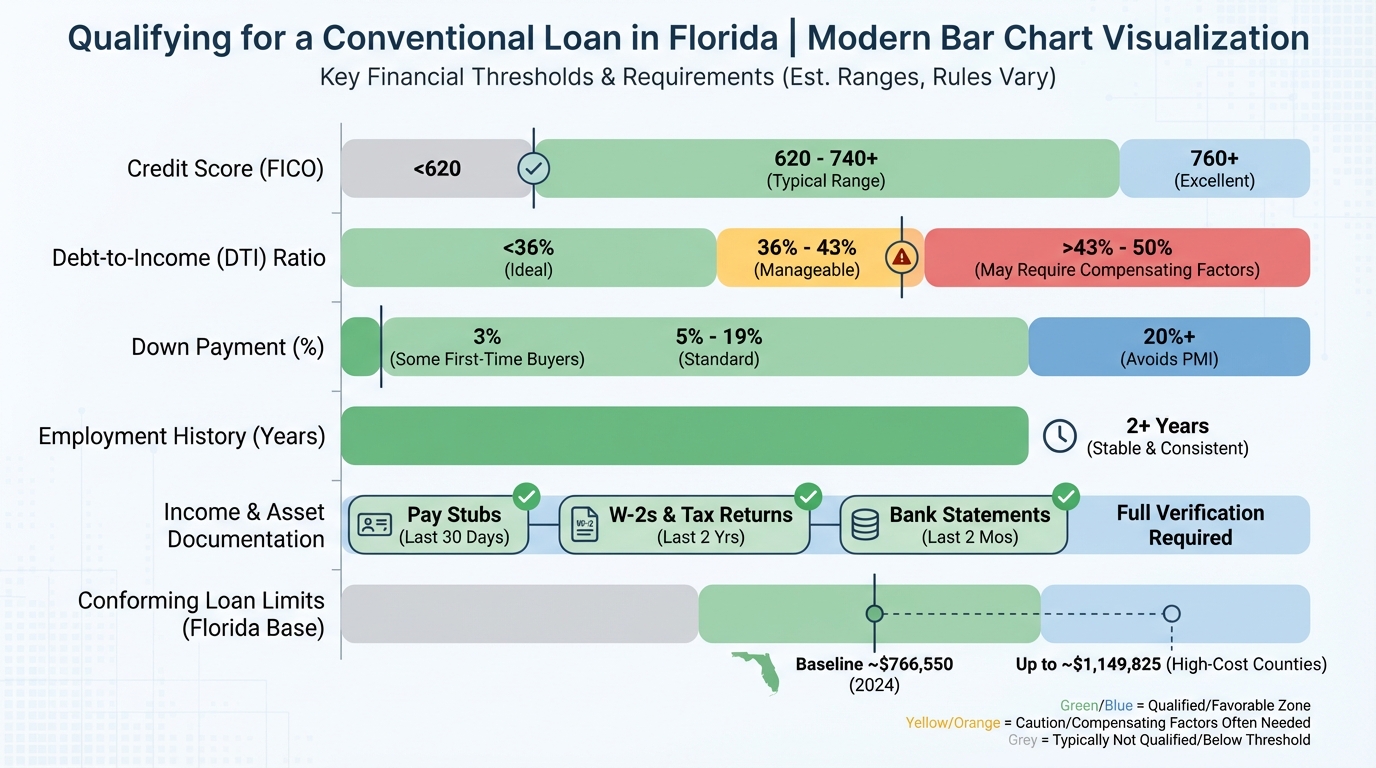

Qualifying for a Conventional Loan in Florida

Credit Score

The benchmark minimum credit score for a conventional loan is usually 620. However, to secure the most competitive interest rates, a score of 740 or higher is ideal. At The Orlicki Group, we work with you to analyze your credit profile and determine which loan products fit your specific score tier.

Debt-to-Income Ratio (DTI)

Your DTI ratio compares your monthly debt payments (credit cards, student loans, car notes) to your gross monthly income. For conventional loans, lenders typically prefer a DTI of 43% or lower, though some automated underwriting systems may approve ratios up to 50% for borrowers with strong cash reserves and high credit scores.

Loan Limits

Because conforming loans are purchased by Fannie Mae and Freddie Mac, they are subject to loan limits set by the Federal Housing Finance Agency (FHFA). In 2024, the baseline conforming loan limit for a single-family home in most of Florida, including Hillsborough and Pinellas counties, is $766,550.

If you need to borrow more than this amount to purchase a luxury property in Tampa, you would likely need a Jumbo Loan, which is a type of non-conforming conventional loan with its own set of stricter guidelines.

Why Tampa Sellers Prefer Conventional Offers

Why? Because conventional loans generally have slightly more lenient appraisal standards regarding the property’s physical condition. Sellers worry that an FHA appraiser might flag minor issues (like peeling paint or a loose handrail) that must be fixed before closing. A conventional buyer is perceived as having stronger finances and a higher likelihood of closing the deal smoothly without demanding extensive repairs.

If you are in a bidding war in a hot neighborhood like Hyde Park or Seminole Heights, having a conventional pre-approval letter from a reputable local broker like The Orlicki Group can give you a distinct edge.

The Orlicki Group Difference: Tailored Mortgage Solutions

Choosing the right loan program is only half the battle; choosing the right partner to guide you through the process is equally important. At The Orlicki Group, we are leading the change in residential financing by focusing on relationships, not just transactions.

Why work with us?

- Independent Advocacy: As independent mortgage brokers, we do not work for a specific bank. We work for you. We shop dozens of lenders to find the rates and terms that fit your unique financial picture.

- Local Expertise: We are deeply rooted in the Tampa Bay community. We understand the local market nuances, from condo association requirements in downtown to insurance considerations on the coast.

- Education First: We believe an educated borrower is an empowered borrower. We take the time to explain the difference between fixed and adjustable rates, how PMI works, and how to strategize your down payment.

Whether you are a first-time homebuyer or looking to refinance, our mission is to provide honest, open, and expert guidance.

Frequently Asked Questions (FAQs)

1. What is the minimum credit score required for a conventional loan?

Generally, lenders require a minimum FICO score of 620 to qualify for a conventional loan. However, borrowers with scores of 740 or higher typically receive the best interest rates and lower PMI premiums. If your score is below 620, we can discuss other options or strategies to improve your credit.

2. Can I use a conventional loan to buy an investment property in Tampa?

Yes! Conventional loans are the standard financing method for investment properties and second homes. Keep in mind that interest rates and down payment requirements (usually 15-25%) are typically higher for investment properties compared to primary residences.

3. Is it true that I need 20% down for a conventional loan?

No, that is a common misconception. First-time homebuyers can qualify for conventional loans with as little as 3% down. Repeat buyers can often put down as little as 5%. However, putting down less than 20% will usually trigger the requirement for Private Mortgage Insurance (PMI).

4. How long does it take to close a conventional loan?

Conventional loans are known for their efficiency. On average, a conventional loan can close in 30 to 45 days. At The Orlicki Group, we pride ourselves on fast turn times and proactive communication to ensure you meet your contract deadlines.

5. What happens to my PMI once I pay down my mortgage?

This is one of the best features of conventional loans. Once your loan balance reaches 78% of the original value of your home, the lender is required to automatically terminate your PMI (provided you are current on payments). You can also request cancellation once you reach 80% loan-to-value, typically requiring an appraisal to verify the home’s value hasn’t declined.

Ready to Explore Your Mortgage Options?

Conventional loans remain the most commonly used loan programs for a reason: they offer stability, flexibility, and cost savings for qualified buyers. However, every borrower’s financial situation is unique. What works for your neighbor might not be the perfect fit for you.

At The Orlicki Group, we are here to help you navigate these decisions with confidence. From pre-approval to the closing table, rely on our team for a mortgage experience that is unrivaled in the industry.

Don’t navigate the housing market alone. Let us help you find the loan that fits your life.

Contact The Orlicki Group Today!

Call us at: (813) 302-1616

Email: info@orlickigroup.com

Click here to Request a Quote or Get Pre-Approved

Disclaimer: The Orlicki Group is a mortgage broker based in Tampa, FL (NMLS #205123). All loans are subject to credit approval and meeting specific underwriting criteria. Information provided in this blog post is for educational purposes and does not constitute financial or legal advice. Loan programs, terms, and conditions are subject to change without notice.