Welcome to 2026. As we settle into the new year, the Tampa real estate market continues to evolve. For many prospective homeowners in Hillsborough and Pinellas counties, the conversation around interest rates remains the headline story. While many industry experts predicted aggressive rate cuts by now, the reality has been a bit more stubborn. We are seeing forecasts of limited rate drops, meaning the “wait and see” strategy for a massive plummet in fixed rates might not be the most prudent move for everyone.

In previous years, the 30-year fixed-rate mortgage was the undisputed king of financing. It offered stability in a volatile world. However, as affordability remains a challenge due to sustained property values in areas like Hyde Park, Westchase, and Downtown Tampa, savvy buyers are looking for alternatives. Enter the Adjustable-Rate Mortgage (ARM).

At The Orlicki Group, our mission is to provide honest, open, and expert guidance. We don’t work for the bank; we work for you. Today, we are diving deep into a financial tool that is making a strong comeback: the ARM. Is it the right strategic move for your 2026 home purchase? Let’s explore the data, the risks, and the potential rewards.

The 2026 Mortgage Landscape:Why Look Beyond Fixed Rates?

For the past several years, the standard advice was simple: “Lock in a fixed rate.” When rates were historically low, this made perfect sense. However, in the current 2026 economic climate, the spread between fixed-rate mortgages and adjustable-rate mortgages has widened. This “spread” represents an opportunity for significant monthly savings.

Many Tampa buyers are facing a specific dilemma: home prices have stabilized but remain high, and fixed interest rates are not dropping as quickly as anticipated. This creates a pinch on monthly cash flow. An ARM can act as a pressure release valve, offering a lower introductory interest rate for a set period (usually 5, 7, or 10 years) before adjusting to market rates.

If you are planning to stay in your home forever, a fixed rate provides peace of mind. But statistics show that the average American moves or refinances every 5 to 7 years. If you don’t plan to hold the specific mortgage for 30 years, paying a premium for a 30-year fixed rate might be an unnecessary expense.

What Exactly is an Adjustable-Rate Mortgage (ARM)?

There are many misconceptions about ARMs, largely stemming from the housing crash nearly two decades ago. It is important to note that the lending landscape has changed drastically since then. Today’s ARMs are regulated, transparent, and structured with consumer protections known as “caps.”

An ARM is a home loan with an interest rate that can change periodically. Most ARMs are “hybrid” loans, meaning they have two distinct phases:

- The Fixed Period: For the first few years of the loan (typically 5, 7, or 10 years), your interest rate remains fixed and does not change. This rate is usually lower than the going rate for a standard 30-year fixed mortgage.

- The Adjustment Period: After the fixed period ends, the interest rate can adjust up or down based on market conditions at that specific time.

For example, in a 5/1 ARM, the rate is fixed for the first five years. The “1” means the rate can adjust once every year after that initial period.

Understanding the Safety Caps

One of the most critical features of modern ARMs is the rate cap structure, which limits how much your interest rate can increase. These are typically expressed as three numbers (e.g., 2/2/5):

- Initial Adjustment Cap: The maximum amount the rate can change the first time it adjusts.

- Subsequent Adjustment Cap: The maximum amount the rate can change in each subsequent adjustment period.

- Lifetime Cap: The maximum interest rate the loan can ever reach, regardless of how high market rates go.

The Strategic Advantage for Tampa Homebuyers

Why would a buyer in Tampa, FL choose an ARM in 2026? It comes down to cash flow and strategic financial planning. Here is why an ARM might be relevant for you specifically right now:

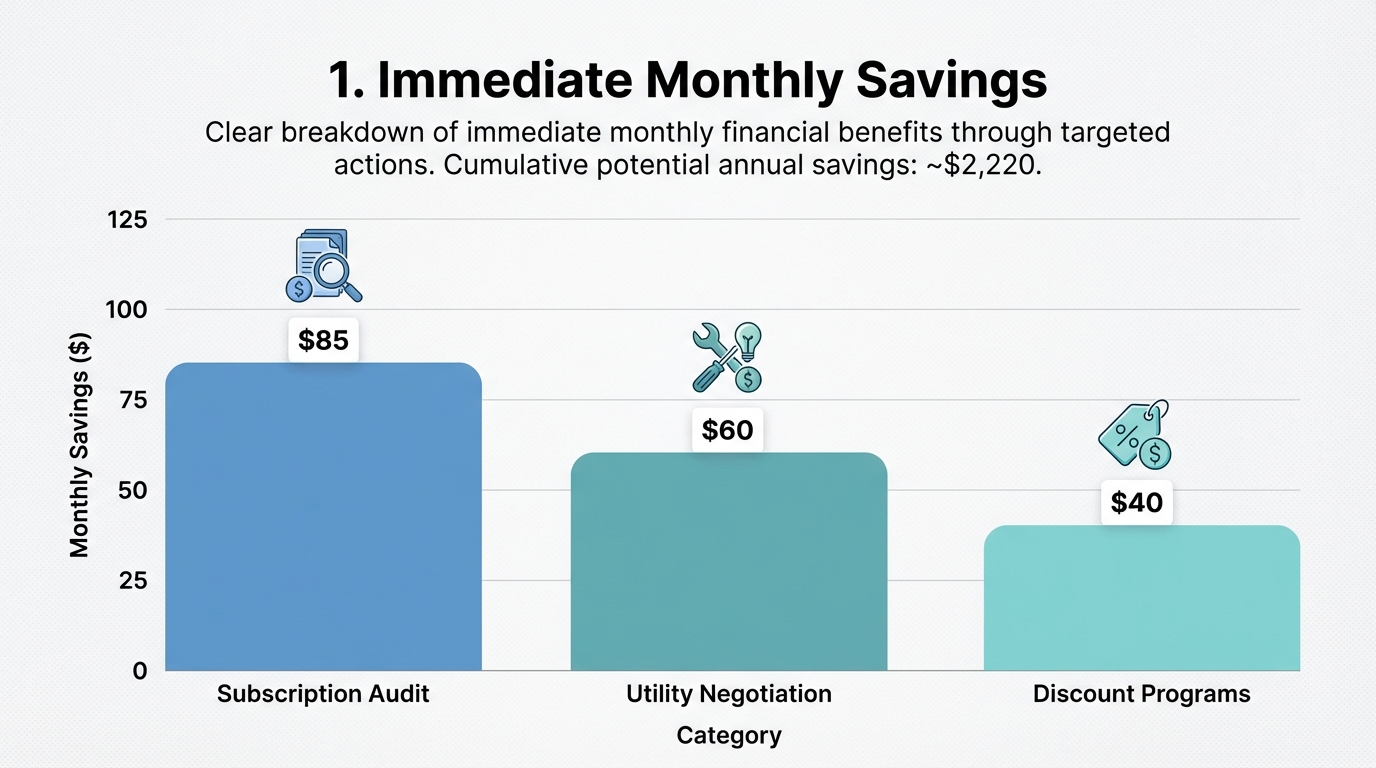

1. Immediate Monthly Savings

2. The “Marry the House, Date the Rate” Strategy

Even with forecasts of limited rate drops, most economists agree that rates are cyclical. By utilizing a 5-year or 7-year ARM, you are essentially betting that within that 5-7 year window, there will be an opportunity to refinance into a fixed-rate loan when rates eventually dip. You get the lower payment now, with the intention of securing a permanent rate later.

3. Short-Term Homeownership Plans

Visualizing the Savings: Fixed vs. ARM

To illustrate the potential impact, let’s look at a hypothetical scenario for a home purchase in the Tampa Bay area. Please note that these figures are for educational purposes only and do not constitute a loan estimate.

| Loan Scenario | 30-Year Fixed Rate | 5/1 Adjustable-Rate Mortgage (ARM) |

|---|---|---|

| Loan Amount | $450,000 | $450,000 |

| Hypothetical Interest Rate | 6.5% | 5.75% |

| Principal & Interest Payment | $2,844 | $2,626 |

| Monthly Savings | $0 | $218 |

| Annual Savings | $0 | $2,616 |

| Savings Over 5 Years | $0 | $13,080 |

*Rates used are hypothetical examples for comparison only. Actual rates vary based on credit score, loan-to-value ratio, and daily market changes. Contact The Orlicki Group for a personalized quote.

As the table demonstrates, the savings over the initial fixed period can be substantial—enough to cover renovations, build an emergency fund, or simply enjoy the Tampa lifestyle.

The Risks: Is an ARM Right for You?

The main risk of an ARM is “payment shock.” If interest rates skyrocket and you are unable to refinance or sell your home before the fixed period ends, your monthly payment could increase significantly once the loan adjusts. However, thorough qualification and financial planning can mitigate this risk. We help you analyze the “worst-case scenario” so you are never caught off guard.

Why Work with a Local Mortgage Broker?

Choosing the right mortgage is not just about picking a product; it is about choosing a partner. As a local independent mortgage broker serving Tampa, FL, and the surrounding states, The Orlicki Group offers distinct advantages over big-box banks.

- We Shop for You: We are not tied to one lender. We work with a network of top lenders to find the specific ARM or fixed-rate product that fits your unique financial picture.

- Tailored Solutions: We understand that every borrower is different. Whether you are a first-time homebuyer, self-employed, or a jumbo buyer, we customize the loan to fit your needs.

- Local Expertise: We know the Tampa market. We understand the nuances of condo financing in downtown or flood insurance requirements in coastal areas, ensuring your loan process is smooth.

- Relationship Driven: As Oliver Orlicki, our founder, says, “We focus on relationships, which often get overlooked in this industry.” We are here to educate and advocate for you from pre-approval to closing and beyond.

Frequently Asked Questions (FAQs)

1. Are Adjustable-Rate Mortgages safe in 2026?

Yes, modern ARMs are much safer than the products seen prior to 2008. They now come with strict federal regulations and caps that limit how much your interest rate can increase per year and over the life of the loan. However, they do carry interest rate risk after the fixed period ends, so they are best suited for borrowers with a strategy to sell or refinance.

2. Can I refinance an ARM into a fixed-rate mortgage later?

Absolutely. In fact, this is the most common strategy. Most borrowers take an ARM to save money during the initial years and then refinance into a fixed-rate mortgage when market rates drop or before their ARM begins to adjust. We offer a Refinance Analysis to help you time this move perfectly.

3. How much can my interest rate go up with an ARM?

This depends on your specific loan terms, known as the “caps.” For example, a common cap structure is 2/2/5. This means your rate cannot increase by more than 2% at the first adjustment, 2% at any subsequent adjustment, and never more than 5% above your initial start rate over the lifetime of the loan.

4. Is an ARM a good idea for a first-time homebuyer in Tampa?

It can be. First-time buyers often have tighter budgets, and the lower monthly payment of an ARM can make qualifying easier or allow them to afford a slightly better home. Since many first-time buyers move up to a larger home within 7 years, an ARM often aligns perfectly with their timeline.

5. What is the difference between a 5/1 ARM and a 7/1 ARM?

The first number refers to the number of years the interest rate is fixed. A 5/1 ARM has a fixed rate for 5 years, while a 7/1 ARM is fixed for 7 years. Generally, the shorter the fixed period (e.g., 5 years vs. 7 years), the lower the introductory interest rate will be.

Ready to Explore Your Mortgage Options?

Navigating the 2026 housing market requires a strategic partner. Whether you are considering an ARM to maximize your buying power or prefer the stability of a fixed-rate loan, The Orlicki Group is here to help you make an informed decision.

Don’t let uncertainty about rates keep you from your dream home. Let us run the numbers for you. We can provide a detailed comparison of fixed vs. ARM options tailored to your specific budget and goals.

Get started today by using one of our free tools or reaching out to our team directly.