Welcome to 2026. The real estate landscape has evolved, and for residents in Tampa, St. Petersburg, and across Florida, the opportunities to build wealth through homeownership have never been more dynamic. Whether you are looking to purchase your first home, leverage equity from an existing property, or navigate the complexities of self-employed income, having a strategic roadmap is essential.

At The Orlicki Group, we believe that finding the right mortgage shouldn’t be a headache. As a local, independent mortgage broker, our mission is to inspire change in residential financing by prioritizing relationships over transactions. We don’t work for the banks; we work for you. This guide serves as your comprehensive roadmap for 2026, tailored to help you navigate the market with confidence, clarity, and the best financial tools available.

1. The 2026 Tampa Housing Market: A Landscape of Opportunity

The Tampa Bay area continues to be a hub for growth, attracting families, professionals, and investors alike. As we settle into 2026, the market demands a more sophisticated approach to financing. It is no longer enough to simply “get a loan.” You need a mortgage strategy that aligns with your long-term financial goals.

Unlike big retail banks that fit you into a rigid box, The Orlicki Group shops dozens of lenders to find the specific product that fits your life. Whether you are eyeing a condo in Downtown Tampa, a family home in Westchase, or a beachfront property in St. Pete, understanding your financing options is the first step toward success.

2. Strategic Buying: finding the Right Loan for Your Life

One of the biggest misconceptions in 2026 is that you need a “perfect” 20% down payment and a W-2 job to buy a home. While those things help, the modern mortgage market offers incredible flexibility. Here is how we are helping different types of buyers succeed this year:

For the First-Time Home Buyer

Entering the market for the first time is a milestone. In 2026, affordability and cash-to-close remain top concerns. We specialize in structuring loans that minimize your upfront costs while keeping monthly payments manageable.

- FHA Loans: Ideal for buyers with credit scores as low as 580, requiring only 3.5% down. This is a powerful tool for getting into the market sooner rather than later.

- Conventional Loans: For those with stronger credit, we can often secure conventional financing with as little as 3% down, offering a great pathway to building equity without the upfront burden of a massive down payment.

- VA Loans: We are honored to serve our veterans in the Tampa area. VA loans offer 0% down payment options and no monthly mortgage insurance, making them arguably the best loan product available.

If you are unsure where to start, our team offers a comprehensive mortgage walkthrough to educate you on every step of the process.

For the Self-Employed and Business Owner (Non-QM Loans)

If you are a freelancer, gig worker, or business owner in St. Petersburg or Tampa, you know the struggle: you make great money, but your tax returns show a different story due to write-offs. In the past, this meant a loan denial. In 2026, we have a solution.

We specialize in Non-QM (Non-Qualified Mortgage) loans. These are designed specifically for borrowers who do not fit the standard government-backed mold. We can verify your income using:

- Bank Statement Loans: We review 12 to 24 months of personal or business bank statements to calculate your true cash flow, rather than looking at your taxable income.

- Profit & Loss (P&L) Statements: A statement prepared by your CPA can be used to verify income, bypassing the need for complex tax return analysis.

- Asset Depletion: High-net-worth individuals with significant savings or retirement accounts can use those assets to qualify for a tailored monthly income stream.

Do not let your entrepreneurial spirit prevent you from buying a home. Contact us today to discuss how we can use your real-world income to get you pre-approved.

For the Luxury Buyer (Jumbo Loans)

The luxury market in Tampa Bay is thriving. However, standard loan limits often don’t cover high-value properties. Our Jumbo Loan products are designed for homes that exceed conforming loan limits. As an independent broker, we have access to Jumbo investors who offer competitive rates and flexible terms that big banks simply cannot match. We can help you secure the financing needed for your dream estate without the red tape.

3. Refinancing in 2026: More Than Just Rate Dropping

Many homeowners view refinancing solely as a way to lower their interest rate. While that is a valid reason, a strategic refinance in 2026 can accomplish much more. We conduct a thorough Refinance Analysis for our clients to determine if a move makes financial sense.

Cash-Out Refinance for Debt Consolidation

With consumer debt rising, using the equity in your home to pay off high-interest credit cards or personal loans can be a game-changer. By consolidating debt into your mortgage, you can often save hundreds—sometimes thousands—of dollars per month in cash flow, even if your mortgage rate is slightly higher than your previous one. It is about the blended rate and total monthly savings.

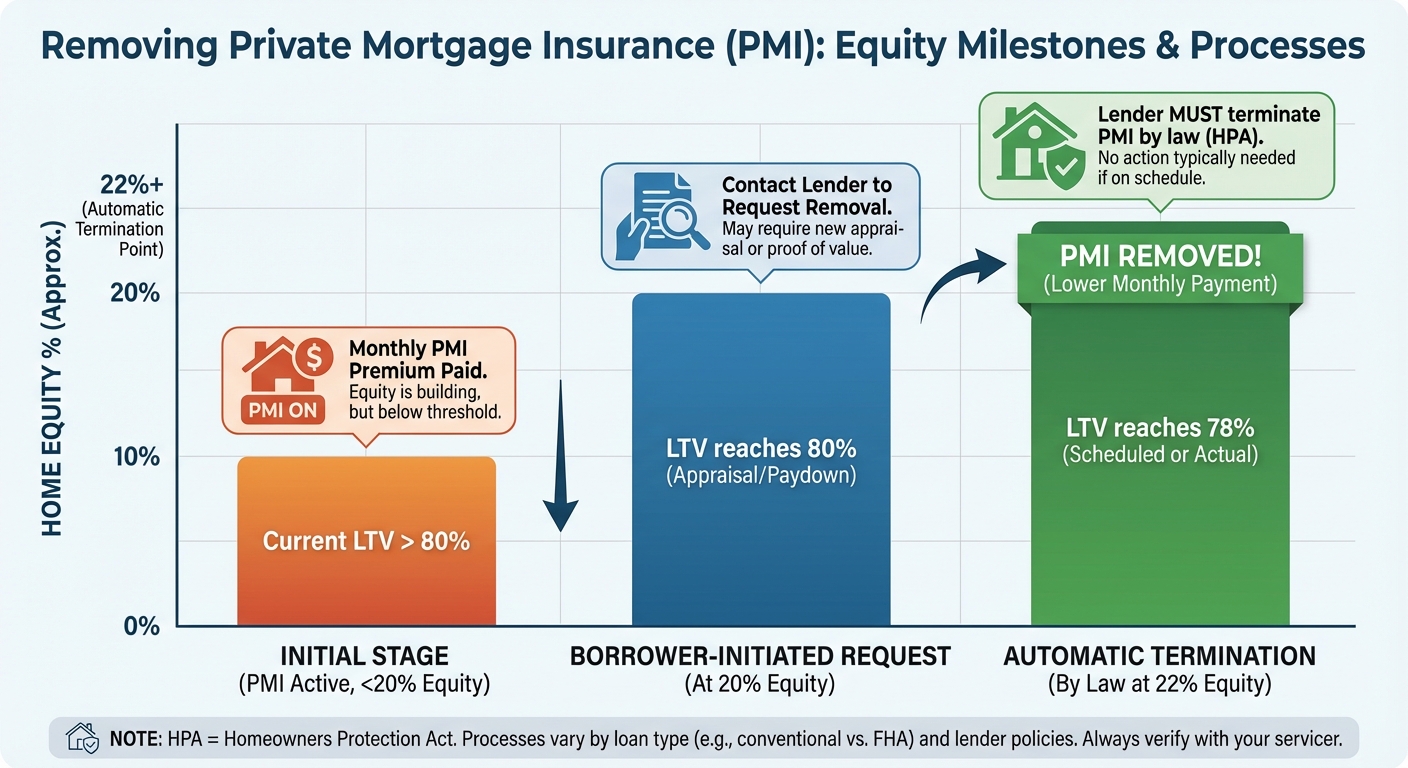

Removing Private Mortgage Insurance (PMI)

Renovation Loans

Love your location but need to upgrade the house? A renovation refinance allows you to borrow against the future value of your home to fund kitchens, baths, or additions. It is often cheaper and easier than selling and buying a new home.

4. Building Wealth: Investment Properties and DSCR Loans

DSCR (Debt Service Coverage Ratio) Loans: These loans are a favorite among our investor clients. We qualify the loan based on the cash flow (rental income) of the property itself. If the rent covers the mortgage payment, you can qualify—often without providing personal tax returns or employment history. This is perfect for scaling a portfolio of rental properties or Airbnb investments in Florida’s tourism hotspots.

5. The Challenge of Buying and Selling Simultaneously

One of the most stressful scenarios in real estate is trying to buy a new home while selling your current one. Timing the closings, moving funds, and managing contingencies can be overwhelming. This is where working with an expert broker makes a difference.

We help coordinate the timing and structure the financing properly. Whether it involves bridge financing tailored to your situation or negotiating specific closing timelines with your real estate agent, we ensure you aren’t left homeless in between transactions. We communicate proactively with all parties—agents, title companies, and lenders—to keep the “dominoes” falling in the right direction.

6. Comparison: Traditional vs. Non-QM Loans

| Feature | Traditional Loans (Conventional/FHA) | Non-QM Loans (Bank Statement/DSCR) |

|---|---|---|

| Target Borrower | W-2 Employees, steady verifiable income. | Self-employed, Investors, Freelancers, Gig Workers. |

| Income Verification | Tax returns, W-2s, Pay stubs (Strict). | Bank statements (12-24 months), P&L, or Rental Income. |

| Credit Requirements | Strict credit score minimums (usually 620+ for Conventional). | More flexible; allows for recent credit events in some cases. |

| Loan Limits | Capped at conforming limits (updated annually). | Higher limits available (Jumbo Non-QM). |

| Flexibility | Low flexibility; must fit government guidelines. | High flexibility; common-sense underwriting. |

7. Planning for the Future: Reverse Mortgages

Our roadmap wouldn’t be complete without addressing our senior clients. For homeowners aged 62 and older, a Reverse Mortgage can be a strategic financial planning tool. It allows you to convert part of the equity in your home into cash without having to sell the home or pay additional monthly bills.

This can be used to supplement retirement income, cover medical expenses, or fund home modifications to age in place comfortably. At The Orlicki Group, we approach Reverse Mortgages with education and care, ensuring it is the right fit for your long-term estate planning.

Frequently Asked Questions (FAQs)

1. I am self-employed with high revenue but low taxable income. Can I still buy a house in Tampa?

Absolutely. This is exactly where The Orlicki Group excels. We use Non-QM products like Bank Statement Loans. Instead of looking at your tax returns, we analyze your business or personal bank statements over 12 to 24 months to determine your true cash flow and ability to repay. This allows you to qualify for a mortgage that reflects your actual earnings.

2. Is it better to use a Mortgage Broker or go directly to a bank?

A local independent mortgage broker like The Orlicki Group works for you, not the bank. Retail banks only offer their own proprietary products. We have access to a vast network of wholesale lenders, allowing us to shop around for the lowest rates, lower fees, and more flexible loan options (like Non-QM and Jumbo) that traditional banks often don’t offer.

3. What is the minimum down payment required for a home in 2026?

It depends on the loan type. For FHA loans, the minimum is 3.5%. For Conventional loans, first-time buyers can often qualify with just 3% down. Veterans using a VA loan can purchase with 0% down. We can help you run the numbers to see which option fits your budget best.

4. Can I buy a new home before I sell my current one?

Yes, but it requires careful planning. We can explore options like bridge loans or specific financing contingencies. We also calculate if you can qualify for both mortgages simultaneously, allowing you to move into your new home before selling the old one, which reduces the stress of moving twice.

5. How do I know if I am ready to refinance?

Refinancing makes sense if there is a tangible benefit, such as lowering your monthly payment, shortening your loan term, removing PMI, or accessing cash for debt consolidation. We offer a free Refinance Analysis where we look at your current rate, equity position, and financial goals to give you an honest recommendation on whether to refinance or hold.

Start Your 2026 Journey with The Orlicki Group

The roadmap to homeownership in 2026 is paved with opportunities, provided you have the right guide. At The Orlicki Group, we combine over 24 years of experience with a modern, relationship-focused approach to mortgage lending. We serve clients throughout Florida, including Tampa, St. Petersburg, and beyond.

Don’t let the complexities of the market slow you down. Whether you are a first-time buyer, a savvy investor, or a self-employed entrepreneur, we have a loan product tailored to your story.

Ready to take the next step?

Get Your Custom Rate Quote Today

Contact Oliver Orlicki and the team at (813) 302-1616 or email info@orlickigroup.com to start the conversation.